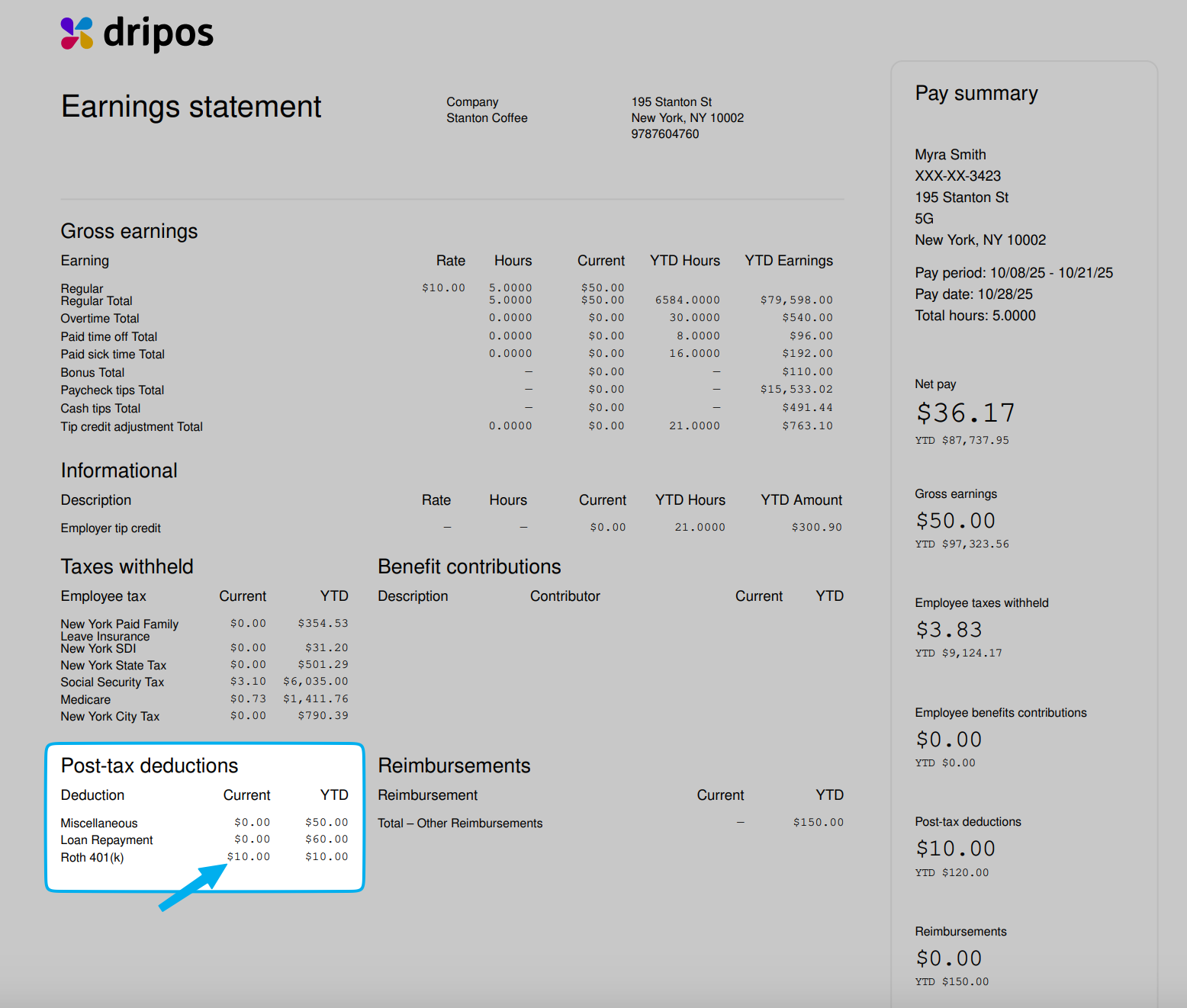

Roth 401(k) Contributions

Contributions to retirement made with post-tax income, allowing for tax-free qualified withdrawals in retirement.

Wage Garnishments

Court-ordered deductions for debts such as child support, student loans, or unpaid taxes. These are mandatory, not voluntary.

Certain Insurance Premiums

Premiums for certain types of life insurance, disability insurance, or voluntary supplemental policies.

Charitable Contributions

Donations made through an employer’s workplace giving program.

Union Dues

Fees paid to a labor union using post-tax income.

Repayment of an Employer Loan or Advance

Wage Garnishments

Employers may need to comply with legal orders from courts, the IRS, and state agencies to withhold portions of employee post-tax or net wages to cover unpaid taxes, child support, alimony or defaulted loans. Types of income that can be garnished include:- Hourly wages

- Salaries

- Commissions

- Bonuses

- Pensions and retirement plan payments

Review these documents carefully.

If you incorrectly process or fail to comply with a garnishment order, your business may face fines or held liable for the employee’s debt.

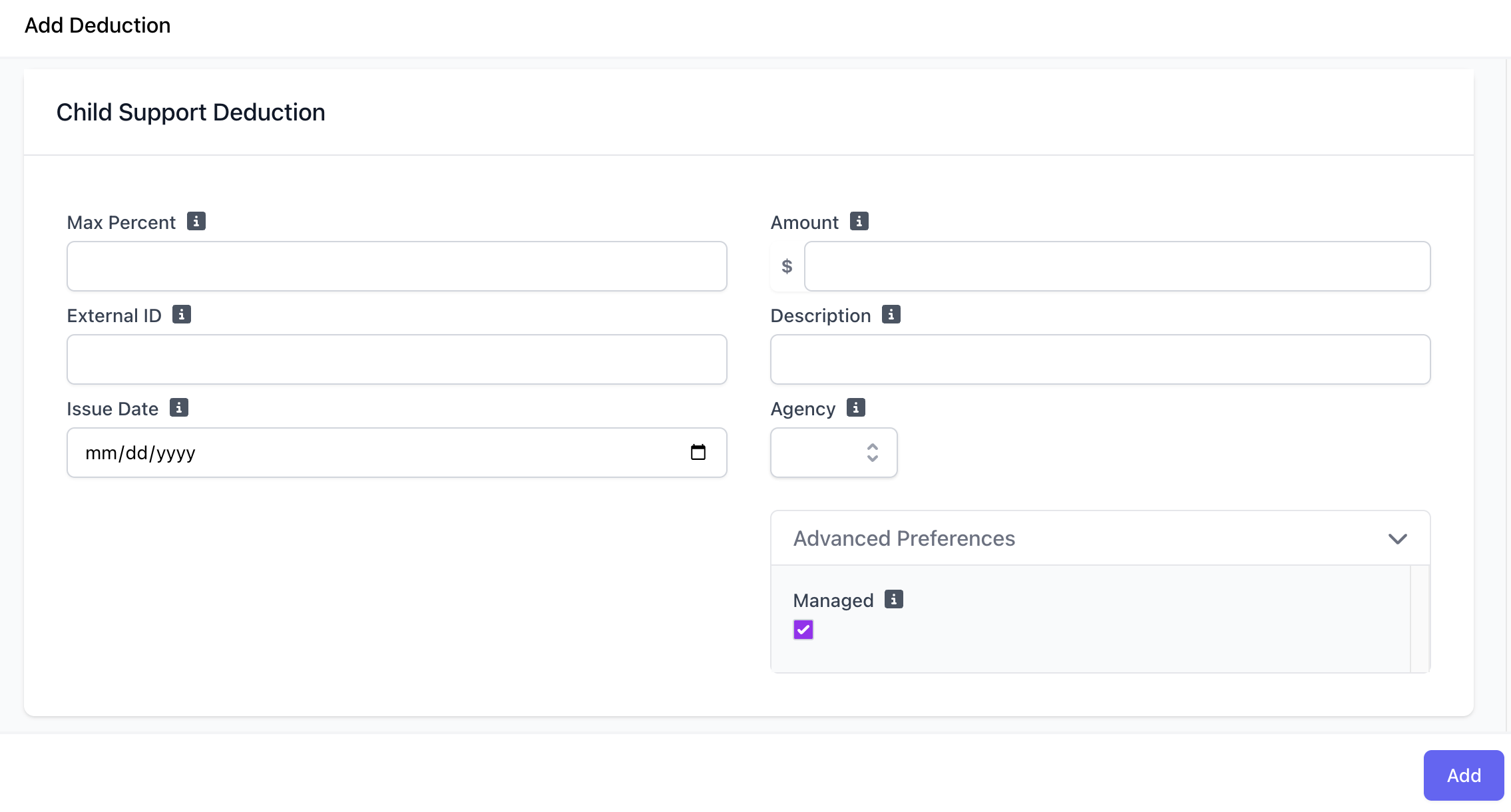

Child Support Post-Tax Deduction

Child support is one of the most common wage garnishiments. Follow the steps below to set up this specific garnishment in Dripos Payroll:1

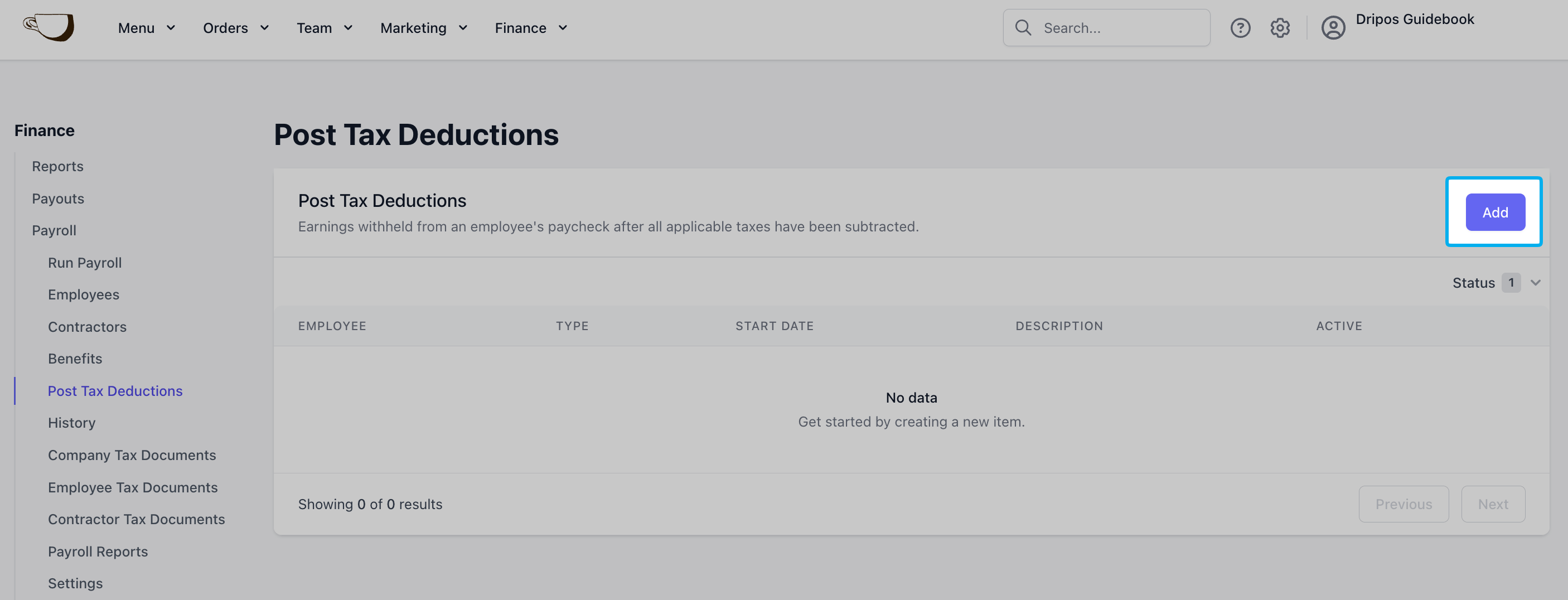

Navigate to Dashboard > Finance > Payroll > Post-Tax Deductions > click Add

2

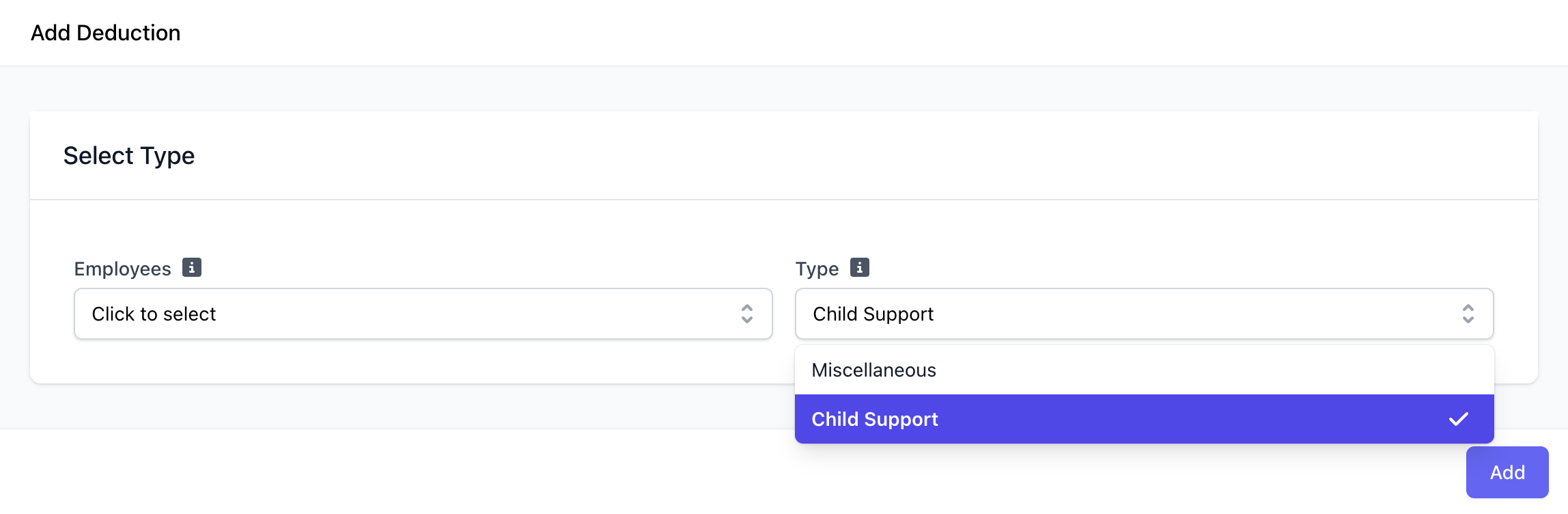

Select the employee to create and apply this Child Support Deduction to. Select the Type as Child Support and click Add.

3

Input the following fields:

Max Percent

Maximum percentage of the employee’s income that will be deducted.

External ID

Unique identifier of the garnishment order, listed as the case number on the order.

Issue Date

Date the collections agency issued the order.

Amount

Per pay period amount to deduct.

Description

Description of the deduction. This is optional but can be helpful for record-keeping.

Agency

Select the state agency that issued the child support.

Advanced Preferences

Select Managed for Dripos Payroll to remit the payment to the appropriate agency on the employer’s behalf.

4

Click Add once the fields are completed. This post-tax deduction will take effect starting on the employee’s next payrun.

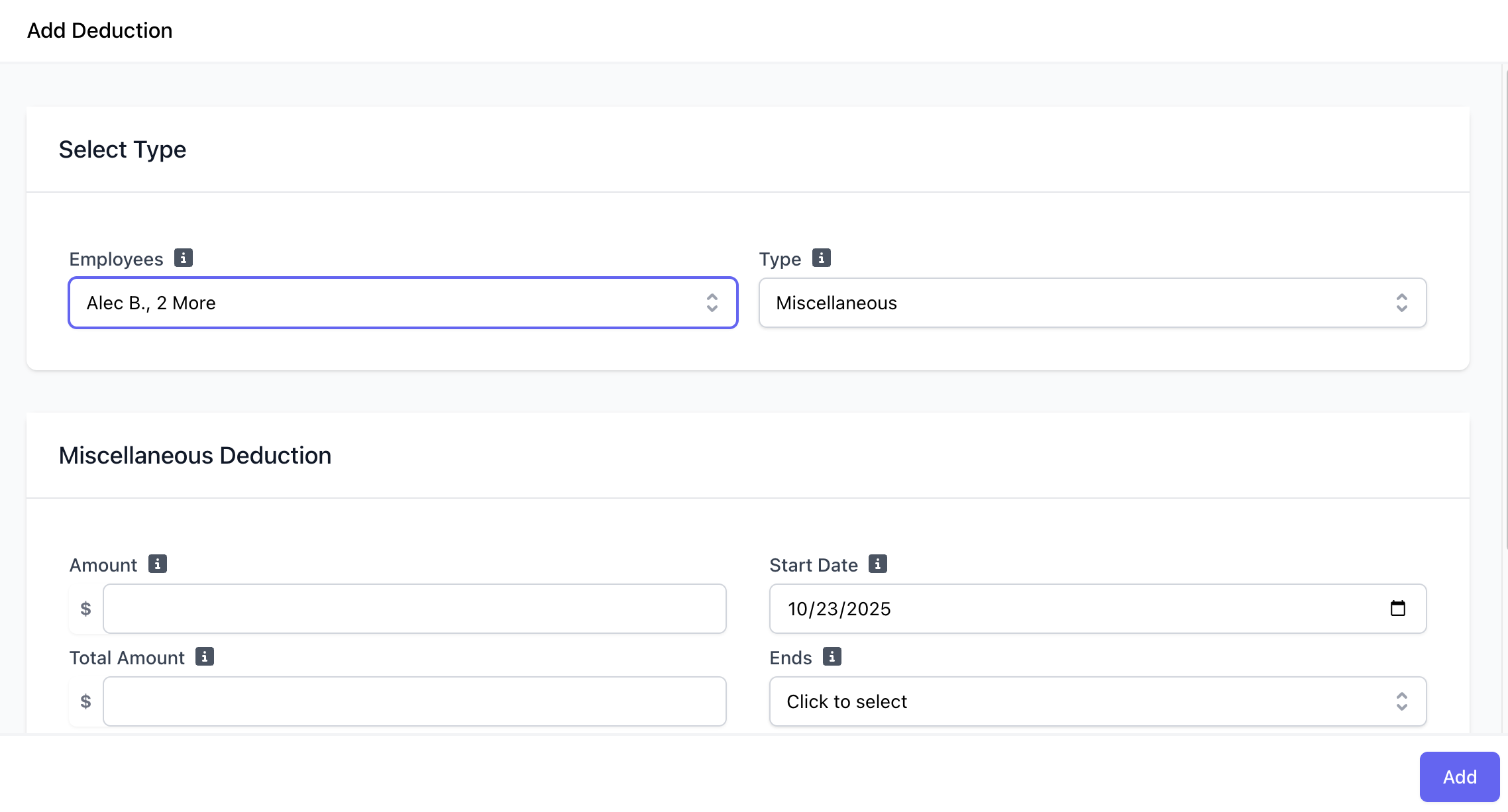

Miscellaneous Post-Tax Deductions

Follow the steps below to create and apply miscellaneous post-tax deductions. Common Examples of Voluntary Post-Tax Deductions:- Roth 401(k) or Roth 403(b) Contributions

- Certain Insurance Premiums

- Union Dues

- Charitable Contributions

- Payments for Other Benefits or Services

Add Miscellaneous Post-Tax Deduction

1

Navigate to Dashboard > Finance > Payroll > Post-Tax Deductions > click Add

2

Select the employee(s) to create and apply this post-tax deduction to. Select the Type as Miscellaneous and click Add.

3

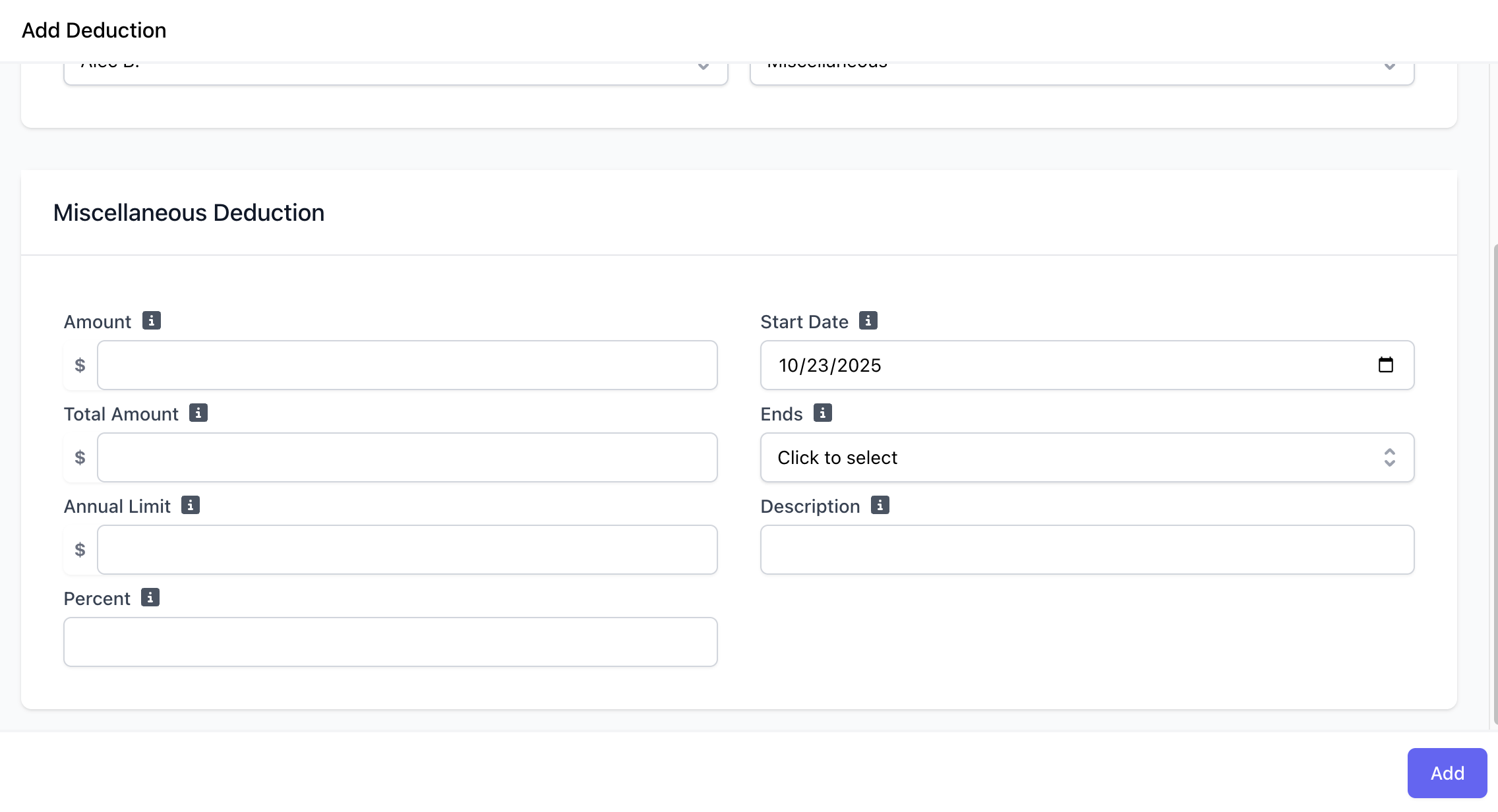

Complete the following fields:

Amount

Fixed dollar amount for the deduction, if applicable. Use either percent or amount.

Total Amount

Total amount applies to the entire effective period of a deduction, which may span multiple payrolls or years if applicable. Use either annual or total limit.

Start Date

Start date for the deduction.

End Date

End date of the deduction. If unsure or indefinite, select Never.

Annual Limit

Annual limit for the deduction, if applicable. Use either annual or total limit.

Description

Description of the deduction. This is optional but can be helpful for record-keeping.

Percent

Percentage of the employee’s income that will be deducted. Use either percent or amount

4

Click Add to create the post-tax deduction.

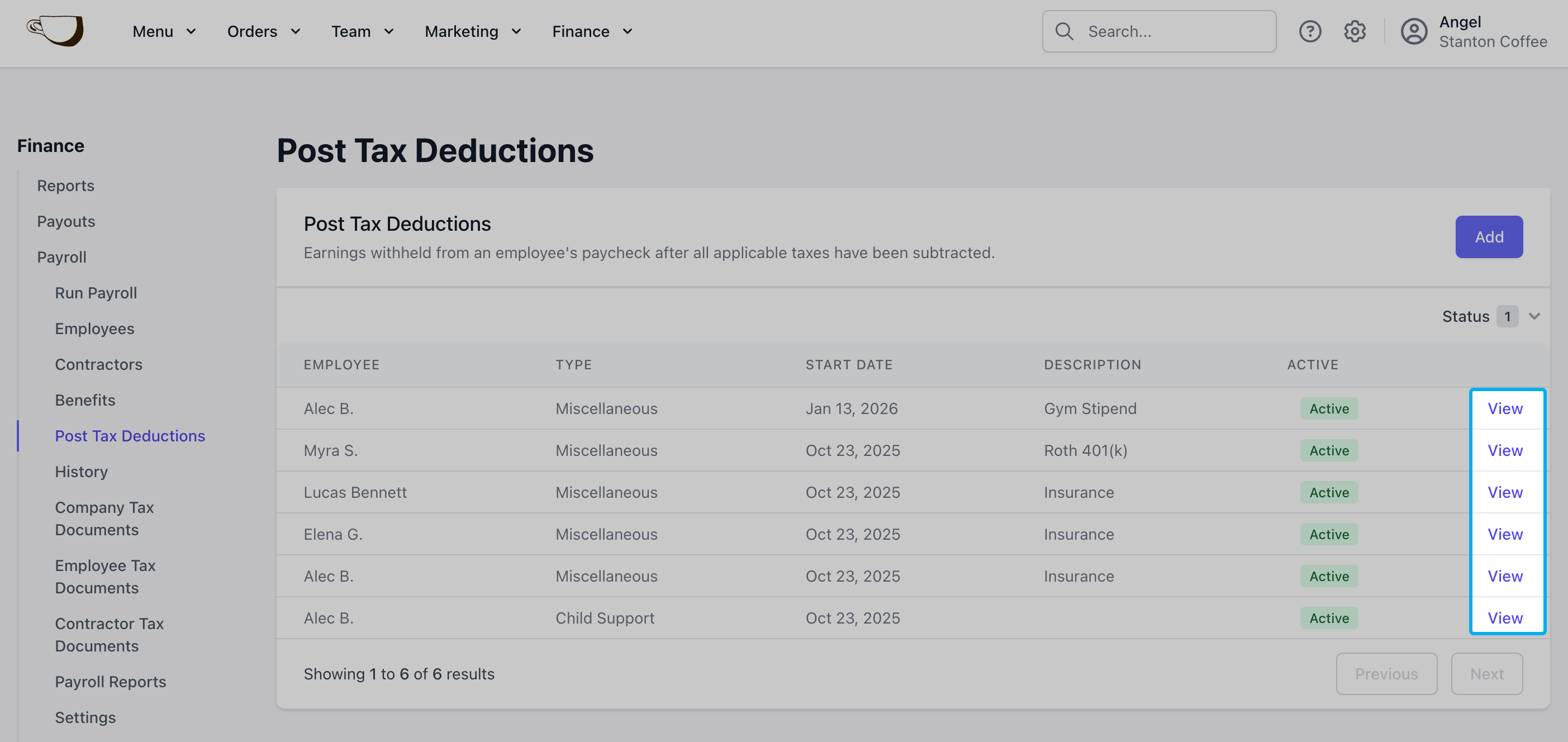

Edit or delete post-tax deductions by clicking View on the applicable employee’s deduction.

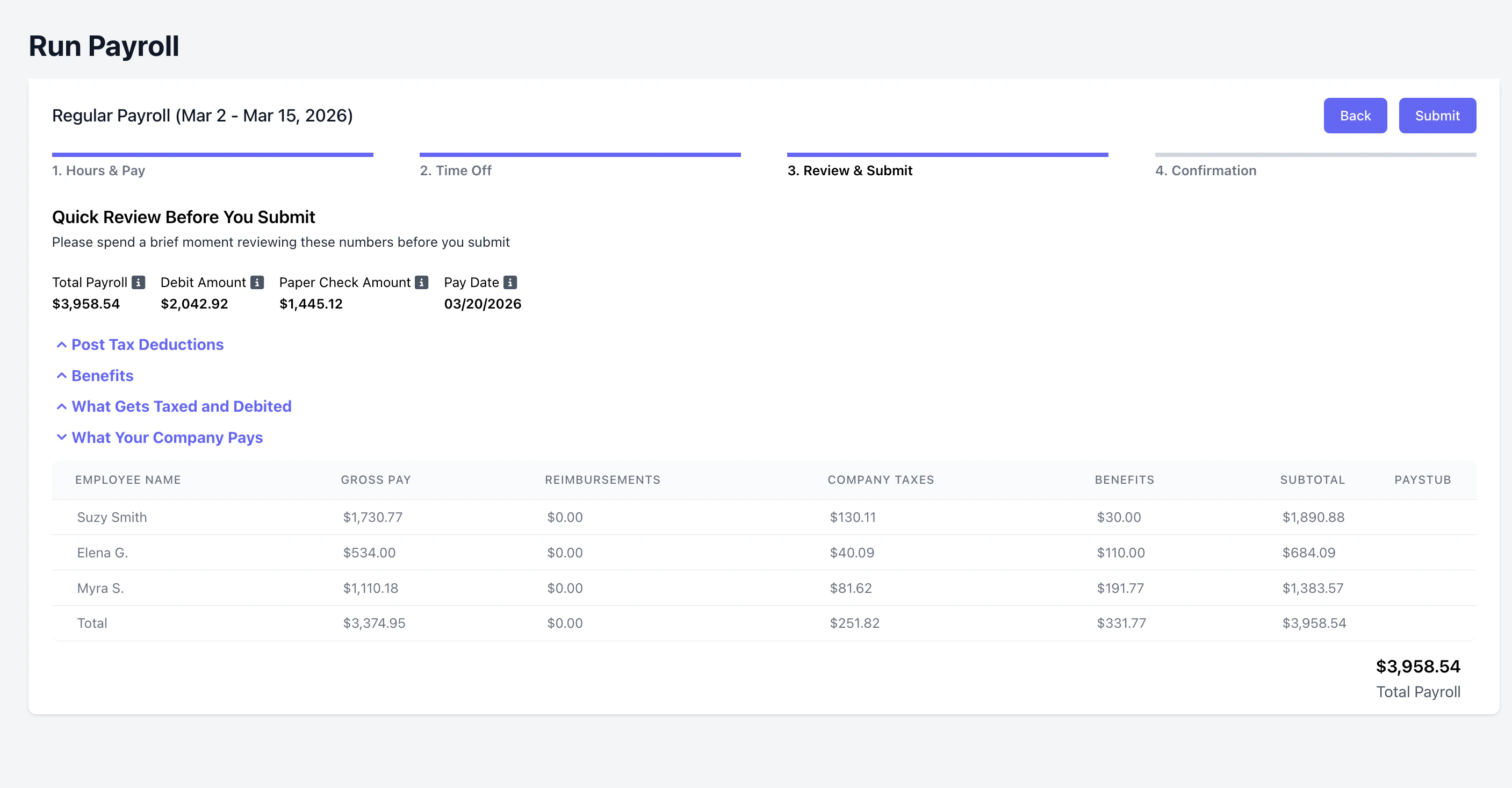

View Post-Tax Deductions in Payroll

Post-tax deductions applied to a payrun will appear on page 3. Review & Submit of payroll. Once payroll is submitted, page 4. Confirmation will also list the post-tax deductions applied.